In the upcoming decades, Slovakia will face rising costs stemming from demographic developments, which will expose public finances to an ever-increasing pressure[1]. One of the main tasks of the Council for Budget Responsibility (“CBR”) laid down in the Fiscal Responsibility Act[2], is to publish the Report on the Long-term Sustainability of Public Finances. The report evaluates whether public policies, in conjunction with the assumed demographic and macroeconomic development, have been set up in a sustainable manner from the perspective of public finances.

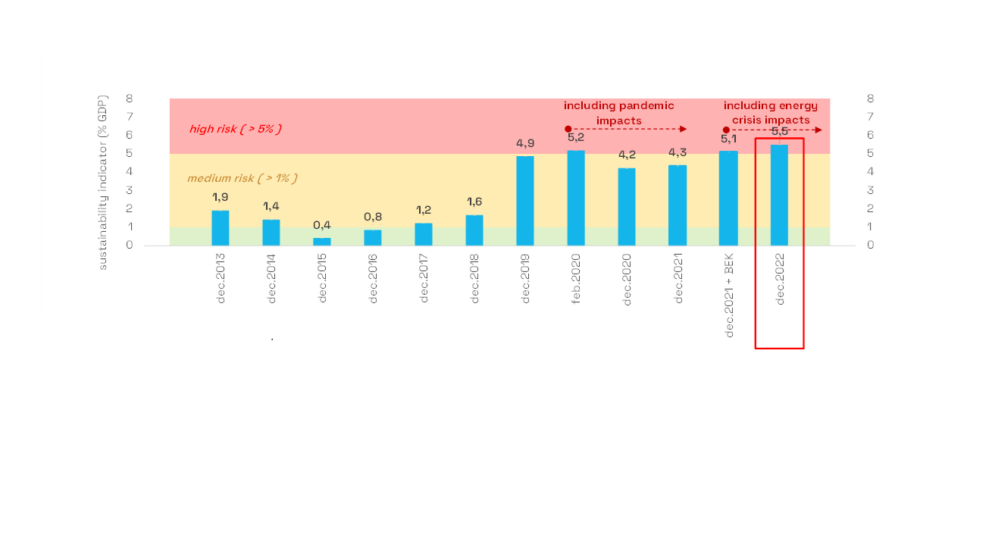

Long-term sustainability of public finances for 2023 is at high-risk

The baseline scenario presented in this report is based on inputs dated at the end of 2023, covering the impacts of measures adopted in 2023. The Council concludes that the long-term sustainability of public finances has again not been achieved in 2023[3]. The long-term sustainability indicator reached 6.2% of GDP[4] (8.1 bn euros), leaving public finances in the high-risk band[5].

The current situation in public finances and pensions, including the outlook for the upcoming years, are among the main causes of problems with long-term sustainability of public finances

In last year’s report, the Council noted that the positive result for 2022 was mainly driven by high inflation rate which led to a sharp rise in general government revenues; however, its effect on expenditures will fully show with a one year delay.

In 2023, the high inflation rate seen in 2022 was indeed fully reflected in the development of public expenditure, which means that the deficit has significantly deteriorated year-on-year. Measures adopted during 2022 and 2023 have also contributed to the increase in deficit. Overall, the fiscal performance in 2023 thus contributes negatively, by 2.2 p.p., to the long-term sustainability of public finances.

As the resulting general government deficit in 2023 is positively affected by factors not carried over to subsequent years (e.g. lower defence spending below 2% of GDP), the balance will deteriorate in the medium term. At the same time, with inflation expected to fall further, the development of public finances will continue to be negatively affected by delayed indexation of expenditure and measures adopted during 2023, contributing negatively to the long-term sustainability by 1.3 p.p. in total.

Beyond the medium term, i.e. between 2028 and 2073, an increase in expenditure sensitive to population ageing will be the main contributor to the negative development in public finances. The largest negative impact, at 1.6 p.p., comes from an increasing deficit in the pension system. Sustainability will also worsen by an additional 1.0 p.p. due to higher health care and long-term care expenditures.

Sustainability worsened primarily due to measures adopted in 2023 and fiscal performance

Compared to 2022, the sustainability of public finances worsened by 0.9% of GDP in 2023, or by 1.3% of GDP if the impact of the change in the second pension system pillar is excluded. The measures adopted had the highest negative effect, at 0.6 p.p., with fiscal performance in 2023 contributing as well (by 0.3 p.p.)[6]. A slightly negative impact on sustainability is also attributable to the projected higher expenditure growth in the medium term, especially when it comes to health care (beyond the measures), which contributed by 0.2 p.p., as well as estimated macroeconomic developments (0.1 p.p.).

Year 2023 saw the adoption of several measures with an overall contribution to the increase in long-term sustainability indicator by 0.6% of GDP (excluding the impact of changes in the second pillar of the pension system):

- Measures in the education sector (funding for research, development and innovation, performance-based contracts in universities, changes in the Schools Act) will contribute, in the medium-term, to the deterioration of the long-term sustainability indicator by 0.5% of GDP. However, in the long-term, these measures may have a positive impact on the potential growth of Slovakia’s economy, thus representing a positive risk for the sustainability of public finances.

- Other factors worsening the long-term sustainability include measures in the health sector (for the most part, an increase in expenditure for health care in hospitals and specialised outpatient care) with an effect of 0.3% of GDP, as well as expenditure-side measures in other areas with a total effect of 0.1% of GDP.

- Regarding the pension system, two legislative measures were adopted, which contributed to the deterioration of the long-term sustainability indicator by 0.2% of GDP. These include, for the most part, increased minimum pensions and a higher percentage rate applied to the loss of capacity for work for selected diseases in terms of disability pensions. The special indexation, hand in hand with the payment of a special 13th pension payment in 2023, have a marginal impact on the long-term sustainability of public finances because they do not permanently increase expenditure for pensions[7].

- On the other hand, the long-term sustainability indicator improved by 0.4% of GDP due to reduction of the second pension pillar contributory rate. The positive impact on long-term sustainability results from the fact that, over a 50-year horizon, the measure has an asymmetrical impact on public finance, in particular, due to the immediate higher revenue of the pay-as-you-go pension system (resulting from the reduced rate paid to the second pillar due to the recent reintroduction of mandatory enrolment for new entrants in the labour market), while an increase in expenditures occurring later is taken into account only partially. Most of the additional expenditure will fully materialise beyond the 50-year horizon.

- The package of measures approved in December 2023 contributed to an improvement in the indicator (beyond the impact of changes in the second pillar which were approved simultaneously) by 0.3% of GDP. In particular, these measures include increased excise duty on tobacco and tobacco products, the introduction of a minimum amount of corporate income tax and extending the special levy on regulated business activity to banks and other entities licensed by the central bank (NBS). A temporary increase of the special levy for banks and a temporary increase of the health insurance contribution by 1 p.p. until 2027 have a negligible impact on the indicator because these measures will expire in three years.

The required consolidation of public finances is postponed due to the non-approval of expenditure ceilings

The current unfavourable condition of public finances requires the necessity to commence the consolidation of public finances as soon as possible. The expected gradually strengthening economic growth, a significant decline in inflation which will temporarily generate a very strong increase in real wages, as well as a gradually recovering external demand are all factors that play in favour of consolidation. In this respect, the fact that the government has not embarked on the permanent consolidation of public finances from 2024 onwards and that expenditure ceilings have not been approved by the parliament in 2024 is regarded very negatively by the Council. The failure to align the budget with the applicable expenditure ceilings[8] constitutes a breach of the Act on General Government Budgetary Rules. The situation in which Slovakia practically does not have an effective instrument in place for the recovery of public finances will thus continue. The unfavourable outlook in public finances is largely attributable to the long-term absence of this instrument[9].

If public finances were consolidated at the level of requirements set by expenditure ceilings[10], three election terms would be needed to achieve the low-risk band of the long-term sustainability of public finances. With a credible consolidation plan, the debt could be stabilised at the Maastricht threshold over the next decade, followed by a gradual decline below 50% of GDP after 2032.

Absence of fiscal space makes Slovakia’s economy vulnerable to possible crises in the future

Slovakia generally faces an external crisis once per decade and, in the past, the domestic economy and public finances coped with such crises significantly worse[11] compared to advanced Western economies, even though Slovakia was enjoying lower debt levels and higher economic growth as opposed to what we are seeing today. If the country were to be hit by a crisis at the beginning of next decade[12], akin to the financial crash (2008 to 2011) or the COVID-19 pandemic (2020 to 2021), the impact on the real economy and public finances could be worse than in the past due to weaker economic growth or worse condition of public finances. Even without a fiscal policy response, such a crisis would almost immediately cause the public debt-to-GDP ratio to rise by 10 percentage points on average; however, by the end of the decade following the crisis, the debt growth would even double due to slow economic recovery and rising risk premiums. The economic losses incurred due to the crisis would be permanent; a decade after the crisis, the economy would have lost about 13 percent of its potential compared to the no-crisis scenario.

Estimating the safe debt level and the probability of default

General government gross debt reached 56% of GDP at the end of 2023. Considering the high deficit estimates and assuming that no additional measures would be adopted, it will subsequently start to increase and exceed the Maastricht criterion of 60% of GDP in 2026. In 50 years, the debt projection under the no-policy-change scenario would reach 417% of GDP. The increase in debt is mainly attributable to the adoption of legislative measures that permanently increase expenditures, as well as to an increase in expenditure sensitive to population ageing. This is a hypothetical scenario because markets would stop financing Slovakia’s needs already at much lower debt levels. In fact, when the state departs from a credible fiscal policy and the risk of its default increases, interest rates in the form of risk premiums will start rising as well. From the perspective of the long-term sustainability, it is therefore key to ensure that the current debt levels are kept as low as possible, so that the debt would remain at a “safe level” even after considering the risk of increased risk premiums in the future.

A debt ratio staying significantly above the safe level for a prolonged time is associated with an increased risk of downgrading the rating to the non-investment grade unless measures are taken to improve the long-term sustainability of public finances. According to the Council’s most recent estimate, the safe level for the net debt is 46% of GDP, but its current level is higher today.

Public debt is now in a high-risk band regarding maintaining the current rating at its current level over the long term. This could lead to a sharp rise in risk premiums, triggering a snowball effect with debt growing significantly above today’s projections. In 2023, the risk of default on long-term liabilities when they become due reached 14 percent. If sufficient consolidation measures are not adopted, the risk of default can be expected to rise sharply after 2026, while more significant problems with the financing of public debt in the financial markets could occur as early as after two election terms[13] (beyond 2031).

Assuming credible consolidation in line with expenditure ceilings, the Council estimates that the risk of default would start falling almost immediately at a faster pace compared to the baseline scenario. When coupled with debt stabilisation, the probability of default could reach 5% already at the horizon of a single election term. In terms of a safe debt level, this would mean that the debt is stabilised at around 55% of GDP. The net debt under this scenario would decline below the upper bound of the safe debt level already after a single election term. Thanks to consolidation, debt interest payments would fall below today’s levels over the period of the next decade and the real economy would be in a better shape than without it[14]. Economic growth would be rising about 0.15 p.p. faster compared to the baseline scenario (without consolidation).

Fiscal burden shifted onto future generations

The results of generational accounts indicate a shift of the fiscal burden onto future generations. While a child born today (in year 2023) will receive 100,000 euros more from public budgets than they will actually pay over their life, the future generations would be facing an opposite situation, contributing 60,000 euros more than what they receive in case that they would have to pay all the liabilities of the current age cohorts (including the existing debt).